This week, the total inventory of construction steel declined, with rebar inventory decreasing by 5.13% WoW and wire rod inventory increasing by 2.35% WoW. On the supply side, although three steel mills had blast furnace maintenance plans this week, the overall operating rate of blast furnaces remained at a relatively high level. Currently, production among EAF steel mills is diverging. In the southwest region, due to electricity subsidies, market profitability has recovered, prompting some electric furnace mills to extend their operating hours. In the south China region, affected by rainy weather and difficulties in collecting steel scrap, overall profitability is poor, leading some severely loss-making electric furnace mills to slightly reduce their operating hours. On the demand side, influenced by positive news from tariff and trade negotiations, macro sentiment has improved, and market speculative demand has recovered. This week, driven by the combined effects of supply-side production structure adjustments and a rebound in market demand, the inventory of construction materials shifted from increasing to decreasing.

This week, the total rebar inventory stood at 5.8283 million mt, decreasing by 315,100 mt WoW, a decline of 5.13% (previous value: 1.65%). Compared to the same period of the lunar calendar last year, it decreased by 1.4886 million mt, a decline of 20.34% (previous value: -20.38%).

Table 1: Overview of Rebar Inventory

Data source: SMM

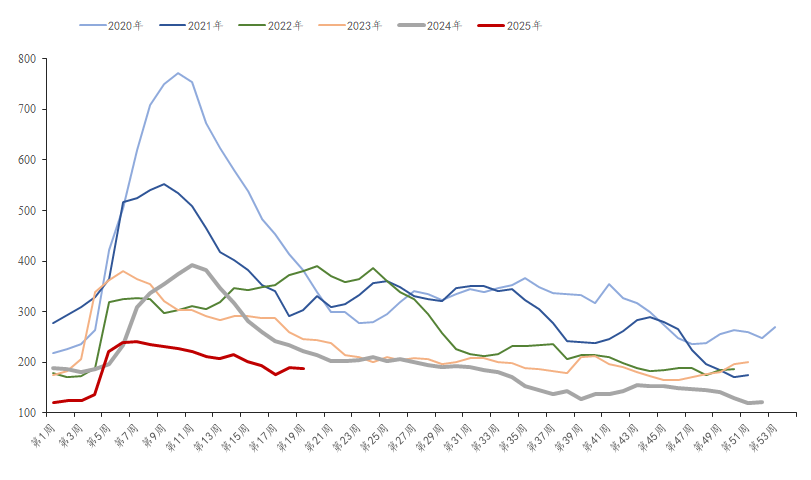

This week, the in-plant inventory of rebar was 1.8756 million mt, decreasing by 31,700 mt WoW, a decline of 1.66% (previous value: 8.6%). Compared to the same period last year, it decreased by 152,100 mt, a YoY decline of 7.5% (previous value: -10.68%). This week, three steel mills had blast furnace maintenance plans, leading to a decrease in overall supply levels. Coupled with the good direct supply situation of steel mills, the in-plant inventory of construction materials decreased.

Chart-1: Overview of Rebar Inventory Trends in Steel Mills, 2020-2025

Data source: SMM

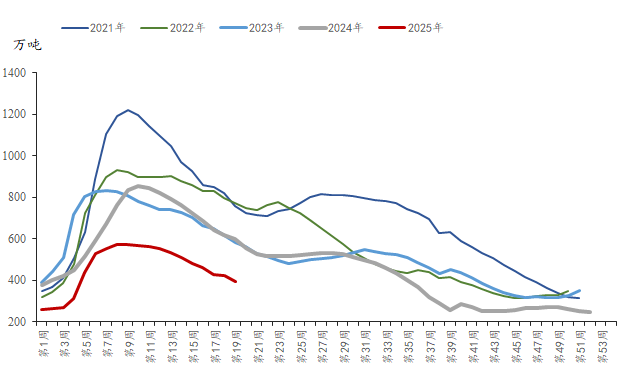

This week, the social inventory of rebar was 3.9527 million mt, decreasing by 283,400 mt WoW, a decline of 6.69% (previous value: -1.2%). Compared to the same period last year, it decreased by 1.3365 million mt, a YoY decline of 25.27% (previous value: -24.09%). This week, substantive progress was made in the China-US talks, leading to a rapid increase in futures steel prices, an improvement in market sentiment, a better trading atmosphere, and an increase in transaction volumes. As a result, the social inventory continued to decline this week, with the rate of decline expanding.

Chart-2: Overview of Rebar Social Inventory Trends, 2021-2025

Data source: SMM

Overall, with the consensus reached in the China-US economic and trade negotiations, positive macro news has boosted market sentiment, and speculative demand has recovered, accelerating the de-stocking of construction materials. However, considering that the peak season in mid-year is drawing to a close and the rainy season has arrived in south China, the sustainability of downstream demand is insufficient, and further contraction is expected in the future. The short-term improvement in sentiment may not be able to sustainably drive up steel prices. Therefore, it is expected that steel inventory will decrease next week, but the rate of decline will significantly narrow.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)